THE HOLE

Everyone is waiting for private credit to unwind. The smart money is patient. They see the leveraged loans, the zombie companies, the marks that have not moved in three years. They think they understand the risk. They are watching the wrong bomb.

Private credit is the fuse. The bomb is underneath the life insurance industry. And it is bigger than the Global Financial Crisis.

"Financial regulators are like archaeologists — they will tell you after the company collapsed what the problem was."— Jim Chanos

I wrote to Secretary Bessent about private credit. About $13 trillion that marks its own homework. About a fund with a higher Sharpe ratio than Bernie Madoff on a portfolio of leveraged loans to zombie companies. About how the machine does not need performance — it needs assets.

I wrote to Speaker Johnson about insurance. About Athene's 9,612-page filing. About how a 419% Risk-Based Capital ratio translates to 69:1 leverage and a 1.45% margin of solvency. The traditional life insurance industry operates at 10 to 15:1. MetLife runs at 11:1. New York Life at 9:1. Athene runs at 69:1. About PHL Variable's $2.2 billion hole. About 602 state examiners overseeing $9.3 trillion. About $1.1 trillion sitting offshore in Bermuda and the Caribbean, in entities whose filings no US examiner can compel.

An insurance company pays another company to take on some of its risk. That is reinsurance. If the first company cannot pay its claims, the reinsurer steps in. It is the backup. The entire system depends on the backup being real. The US life and annuity balance sheet is $10 trillion — 150% of the Federal Reserve’s own balance sheet. The property and casualty side has its own problems — but $10 trillion in life and annuity is a big enough disaster to write about first.

This is about the phantom underneath all of it. The accounting trick so brazen that the NAIC’s — the national body that writes insurance accounting rules — own standards say it is not an asset — and a state legislature passed a special law to make it one anyway. $1.54 trillion in affiliated reinsurance against $657 billion in total industry surplus. Strip the affiliated reinsurance credit from each balance sheet and 29 of the top 30 insurers are insolvent without it. The reinsurance has to be real. If it is not, neither are they. It is crucial that this is good money, but we cannot see it. And what we can see are more liabilities than assets.

Gober has the annual statements of three Vermont captive reinsurers that nobody was ever supposed to see. He has the presentation he gave to the United States Senate Banking Committee. The BIS paper. The IMF note. And four decades of forensic work. He showed me everything.

The industry will compare these numbers to total assets. That is the trick. Total assets includes every bond, every mortgage, every dollar of policyholder money the insurer manages. It is a denominator designed to make any numerator look small. Surplus is the only capital that stands between policyholders and insolvency. Total reinsurance — affiliated and non-affiliated, onshore and offshore — is approximately $2 trillion. Of that, $1.54 trillion is affiliated paper. Not only is the private portion of the $10 trillion US life and annuity balance sheet materially overvalued — a multiple of what was drawn in TARP likely does not exist at all.

I. The Man Who Saw Inside

Thomas D. Gober is a Certified Fraud Examiner and forensic accountant who has spent 41 years inside the life insurance industry. He started as a state examiner in Mississippi in 1985. He spent over a decade working criminal cases with the FBI and the US Attorney's Office. Executives went to prison. Assets were forfeited. He made numerous referrals to the Department of Justice.

In 2009, Newsweek ran "The Next AIG Scandal?" based on his analysis of AIG's 71 interlocking subsidiaries. He brought it to Barney Frank. Frank listened.

In 2022, he submitted findings to the Senate Banking Committee under Sherrod Brown. In 2023, he presented in person to the chief counsel and staff. S. Hrg. 117-747, at 57 (September 8, 2022).

In May 2024, he filed an expert declaration in the Lockheed Martin v. Athene federal lawsuit. Athene's Iowa entity held $155 billion in affiliated reinsurance on a surplus of $2.88 billion. That is 1.44% of assets. TIAA carries 13.83%. New York Life, 12.24%.

Gretchen Morgenson — Pulitzer Prize winner, now with NBC Investigative Reports — had been working the insurance story for months. She called Steve Eisman and told him he had to talk to Gober. On March 2, 2026, Eisman — the man who bet against subprime mortgages and was proved right — brought Gober on his podcast and called the situation "a slow brewing scandal which could be one day a great financial crisis."

I was already neck-deep in Athene's 9,612-page filing when that episode dropped. I was writing my letter to Speaker Johnson about RBC ratios and 69:1 leverage and $114 billion in privately placed bonds. I knew the insurance side was bad. Eisman and Gober turned the fire into an inferno. Everything I had found on the balance sheet — the leverage, the opacity, the offshore cessions — was the surface. What Gober was describing was the machinery underneath. The thing that makes the surface possible.

No one has ever publicly challenged his findings. Not Athene. Not Brookfield. Not the NAIC. Not a single state commissioner. He sent certified letters for years. Return receipt requested. Signature confirmed. Not once did they respond.

For fifteen years he assumed the captives were funded at roughly 70% real assets and 30% phantom. Surely at least 60. Maybe 50.

Then Brookfield screwed up.

The Federal Reserve, the IMF, and the BIS have each arrived at the same destination through their own research. What follows relies on all of them.

II. Three Point Seven Percent

Brookfield acquired American Equity for $4.3 billion. The deal closed in May 2024. They installed themselves as the asset manager.

American Equity had ceded roughly $7 billion in annuity obligations to three wholly owned captives domiciled in Vermont:

AEL Re Vermont, Inc. — formed 2021.

AEL Re Vermont II, Inc. — formed October 2023.

AEL Re Vermont III, Inc. — formed October 21, 2024. Commenced business December 1, 2024.

The third captive was created six weeks before year-end and immediately loaded with $1.5 billion in liabilities. Remember that.

Vermont makes captive financial statements confidential. Even policyholders cannot see them. In 2024 the state eliminated the requirement to disclose even under subpoena. The statements are filed with the Commissioner and locked in a vault.

Brookfield told its technology team to post American Equity's statements online. Someone did not know the captive statements were supposed to stay secret. They posted them. Gober found them and saved copies before they were pulled down. John Ellis broke the story in News Items on November 15, 2025.

AEL Re Vermont, Inc. — the first captive, formed 2021.

| Line | Amount | |

|---|---|---|

| 1 | Bonds | $16,336,555 |

| 2 | Stocks | $23,325,882 |

| 5 | Cash and equivalents | $71,780,904 |

| 8 | Other invested assets | $16,571,624 |

| 12 | Total cash and invested assets | $128,023,546 |

| ...balance sheet is mostly empty... | ||

| 2501 | XOL Asset | $1,480,984,538 |

| Total liabilities | $2,551,890,182 | |

One hundred twenty-eight million dollars in real assets. Then nothing. Empty rows. Until the bottom: an aggregate write-in called “XOL Asset” worth $1.48 billion.

That line is the entire story. An XOL asset is an excess-of-loss reinsurance contract — a promise from a third party to pay if losses exceed a certain threshold. The captive books the value of that promise as an asset. The question is whether the third party will ever pay.

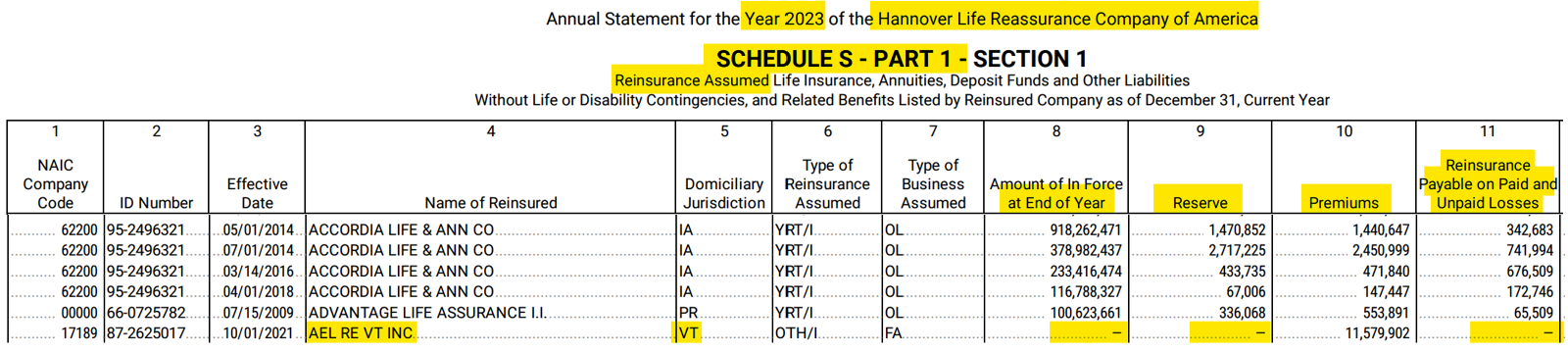

It will not. Gober showed me how to check. Every insurer files a Schedule S. Part 3 lists what it ceded. Part 1 lists what it assumed. The captive’s Schedule S shows it ceded to Hannover Life Reassurance Company of America and booked $1.48 billion. If you go straight to Hannover’s Schedule S Part 1 — the assumed side. The line for AEL Re Vermont Inc. is there. Company Code 17189. Look at columns 9, 10, and 11 — the reserve Hannover booked against this contract, the premium it collected, and the reinsurance payable.

Hannover Life Reassurance Company of America — 2023 Annual Statement, Schedule S Part 1, Section 1. AEL RE VT INC highlighted in yellow. Column 9 (Reserve): dash. Column 10 (Premiums): $11.6 million. Column 11 (Reinsurance Payable): dash.

Reserve: dash. Reinsurance payable: dash. The only number that is not zero is the premium — $11.6 million. That is what Hannover charged for a contract the captive books at $1.48 billion. Flat zeros mean Hannover has determined mathematically that it will never pay. If it believed there was any probability of paying, it would have booked a reserve — even a fraction of $1.48 billion. It booked nothing. The 2022 filing shows the same zeros. It is not a one-year anomaly. Hannover has $577 million in surplus. If this contract were real, Hannover itself would be insolvent. It charged $11.6 million because the only risk it took on was reputational. It collected a fee to pretend.

The captive filed a balance sheet claiming $1.48 billion from Hannover. Hannover filed a balance sheet saying it will pay zero. Both documents are public. Both were filed under oath. This is not a matter of interpretation. It is arithmetic.

The NAIC requires risk transfer tests on reinsurance contracts. Each captive ran them. Every test came back negative. No risk had been transferred. The NAIC’s own accounting standards — SSAP No. 4 — define three characteristics an asset must have. The XOL fails all three. Under the NAIC’s own rules, it is nonadmitted. It should not be on the balance sheet at all.

Vermont’s captive statute has existed for decades — it was designed for legitimate risk management. The industry repurposed it. Vermont permitted XOL assets that fail every NAIC test. Then Vermont made captive statements confidential. Then, in 2024, Vermont made them immune to subpoena. The original law was neutral. What it became is not.

Now look at what those phantoms do to the other two captives.

AEL Re Vermont II, Inc. — formed October 2023. Total real investments: $73 million. XOL Asset: $2.48 billion. Total liabilities: $3 billion. Unassigned surplus without the XOL: negative $2.5 billion. The XOL appears twice — once as an asset, again as “special surplus funds.” Strip it from both sides and the captive is insolvent by $2.5 billion. With it on both sides, the stated surplus is a positive $65 million. That is how you dress up a $2.5 billion hole as a $65 million cushion.

AEL Re Vermont III, Inc. — formed six weeks before year-end. Commenced business December 1, 2024. Immediately loaded with $1.5 billion in liabilities. Total real investments: $60 million. XOL Asset: $1.31 billion. Unassigned surplus: negative $1.3 billion. The ink was barely dry.

| Real Assets | XOL (Phantom) | Total Liabilities | |

|---|---|---|---|

| Vermont I | $128,023,546 | $1,480,984,538 | $2,551,890,182 |

| Vermont II | $73,244,433 | $2,481,454,559 | $2,999,740,612 |

| Vermont III | $59,881,173 | $1,314,385,409 | $1,494,684,166 |

| Total | $261,149,152 | $5,276,824,506 | $7,046,314,960 |

Two hundred sixty-one million dollars in real assets. Seven billion in liabilities. That is 3.7%. Three point seven cents on the dollar.

The phantom doubled in a single year. From $2.56 billion to $5.28 billion. They are not winding this down. They are accelerating.

American Equity’s surplus is roughly $3 billion. The phantom is $5.28 billion. If these captives are representative of how they are funded, the surplus does not exist. Brookfield paid $4.3 billion for a company whose capital is a ledger entry backed by a contract Hannover says it will never honor.

Brookfield calls this vertical integration. It is not vertical. It is circular. American Equity owns 100% of these three captives. It pushed $7 billion in liabilities into entities it wholly owns and sent $261 million in real assets to cover them. Then it told regulators it had eliminated those liabilities. It did not eliminate anything. It moved the claims files from the filing room to the basement. The parent guarantees the captives’ obligations — guaranteeing its own payments back to itself. The FBI has a phrase for transactions that go out and come right back. They call them circular transactions. People have been convicted for this.

Brookfield knew exactly what the XOL was. They tried the same trick on American National — a real insurance company, not a captive, with statements filed publicly with the state. They put an XOL write-in on its balance sheet. It lasted months. Someone noticed. They pulled it off. A bona fide insurance company cannot carry an instrument that fails every definition of an admitted asset. Brookfield knows this. They do it in the captives because nobody can see the captives. A forensic accountant saw this one by accident.

III. Every Time Anyone Looked

The Brookfield leak was not the first time anyone saw inside a captive reinsurer. It was the third.

Scottish Re. A life reinsurer, not a captive — but its affiliated entities used the same structures. Before its collapse, a potential acquirer conducted due diligence.

"We got in there and started digging and we freaked out. Because there was basically nothing there. There was a ton of liabilities, but almost no assets."

PHL Variable. When it entered receivership, the rehabilitator confirmed the XOL assets were worth zero. Policyholders received pennies on the dollar.

Brookfield's Vermont captives. The one time anyone saw inside: 5% funded.

Three glimpses. Three times: almost entirely empty. The rest are confidential.

IV. What They Would Say

The industry has three defenses. They are practiced. They sound reasonable in a conference room. None of them survive contact with the filings.

The first: XOL contracts provide genuine protection against tail risk. The probability of payout is low, but the coverage is real. The booking reflects accepted actuarial methodology. This would be convincing if the captives’ own risk transfer tests had not come back negative. Every one of them. The NAIC requires the test. The captives ran it. No risk was transferred. You cannot simultaneously tell the actuary the contract protects against catastrophic loss and tell the regulator no risk changed hands. There is also a reason the premiums are so cheap. The attachment point — the asset level where the XOL would actually trigger — is typically set below the level at which the insurer would already be in receivership. The contract kicks in after the company is dead. That is why Hannover charges $11.6 million on a $1.48 billion notional. It is not insurance. It is a receipt for a payment that will never come due. Pick one.

The second: captives are adequately supervised by their domiciliary state. This was a stronger argument before Vermont made captive financial statements confidential, eliminated the requirement to disclose them even under subpoena, and locked them in a vault. The supervisor bricked the door shut. If you press the industry for why policyholder money is sitting in Bermuda and Barbados, they will give you the least offensive reason they can find. They will probably say taxes. When the best defense for moving a trillion dollars offshore is that you did not want to pay taxes on it, you have already lost the argument.

The third: affiliated reinsurance is disclosed on Schedule S. Regulators can see it. Investors can see it. The transparency argument. Schedule S shows that Athene has $235.7 billion in affiliated reinsurance on a consolidated basis — reserve credits plus modified coinsurance reserves — structures where the insurer keeps the assets but transfers the risk on paper — across its domestic and offshore entities. It does not show what is backing it on the other side. The only time anyone saw inside a captive, it was funded at 3.7 cents — that was Brookfield. Athene’s captives are confidential. The modco structures are deliberately convoluted — liabilities wrapped in reinsurance wrapped in retrocession — reinsurance of reinsurance —, split across jurisdictions so that no single examiner sees the whole chain. Schedule S shows the door exists. It does not show what is behind it. The disclosure is technically present and practically useless.

And when the chain terminates offshore — in Bermuda, in Barbados, in the Caymans — the United States government has no jurisdiction over what those courts decide. Bermuda has a real regulator. Barbados and the Caymans are lighter. But no offshore jurisdiction has ever been forced to choose between its largest revenue source and American policyholders. We do not know what Bermuda would do. We know what the incentives are. If recovery depends on an offshore court ordering an offshore reinsurer to honor an obligation to an American widow, the outcome is uncertain at best. That is how sovereignty works.

V. $1.54 Trillion

Using NAIC statutory filing data compiled by SNL Financial for year-end 2025, Gober calculated the total affiliated reinsurance — both reserve credits and modified coinsurance reserve taken by US life and annuity carriers on contracts with their own affiliated entities — across all 714 licensed L&A carriers in the United States.

$1,543,722,502,966The entire US life insurance industry reports $657 billion in surplus. Affiliated reinsurance equals 235% of that surplus. The industry has ceded more than twice its total capital to entities it controls — entities in Vermont, Bermuda, Barbados, and the Cayman Islands that file limited or no public financial statements.

Some affiliated reinsurance has legitimate purposes. Tax optimization. Capital efficiency. Risk segmentation. These are bad for the system but they are not fraud. The more troubling reason the number is $1.54 trillion is that once a dollar moves to an affiliate, nobody can verify whether there is anything backing it — or whether it has been reinsured again somewhere else. At the end of this chain, it is likely we would see a lot of nothing.

"$1.54 trillion against 650 billion in total surplus. If even half of this is not good, it breaks everybody. And this is just the affiliated."— Tom Gober

| Entity | Affil Reins | Surplus | Ratio |

|---|---|---|---|

| Athene (Apollo) | $235.7B | $4.1B | 5,719% |

| PICA (Prudential) | $74.5B | $15.9B | 468% |

| RGA Reinsurance | $72.7B | $3.0B | 2,432% |

| John Hancock (Manulife) | $60.9B | $10.5B | 579% |

| Hannover Life Reassurance | $56.9B | $0.6B | 9,857% |

| Pruco Life (Prudential) | $56.5B | $5.8B | 971% |

| Lincoln National Life | $52.7B | $8.0B | 658% |

| Equitable Financial Life | $48.6B | $2.2B | 2,253% |

| Commonwealth Annuity (KKR) | $47.2B | $6.9B | 687% |

| Forethought Life (KKR) | $36.5B | $4.6B | 789% |

| Amer Equity Life (Brookfield) | $35.6B | $2.8B | 1,288% |

| First Allmerica (KKR) | $22.0B | $0.1B | 14,864% |

They will challenge the half. Nobody knows the real number. That is the point — the confidentiality exists so that nobody can know. But after hours of conversation with the one man in the country most qualified to estimate it, I would write a pink slip that the real number is worse than half. And it does not matter. Even at 10% — even if 90% of the affiliated reinsurance is perfectly sound — $154 billion in phantom capital would send dozens of billions in unrecoverable liabilities onto the states. The margin of error they need to be safe does not exist.

Hannover — the entity that writes the XOL contracts it says it will never honor — carries $56.9 billion in affiliated reinsurance on $578 million in surplus. It is leveraged 99 to 1 on affiliated paper. Hannover Re, the German parent, carries over EUR 16 billion in group equity. The industry will point to the parent. The parent may choose to support the US subsidiary. It is not legally obligated to, and in a systemic crisis where the parent itself is stressed, there is no mechanism to compel it. US policyholders have a claim on Hannover Life Reassurance Company of America — the entity that filed the Schedule S with zero reserve and $578 million in surplus. The insurance backing the insurance backing the teacher’s annuity is nothing backing nothing. Turtles all the way down.

Prudential — across three entities — totals $147.2 billion. Apollo/Athene totals $273.6 billion. Global Atlantic, controlled by KKR, totals $113.2 billion.

Athene has $52 billion in affiliated investments — IOUs between brother and sister entities. NAIC guidelines limit affiliated investments to 50% of surplus — $2 billion for Athene. Iowa, as Athene’s domestic regulator, can grant waivers. If Athene has one, the breach is technically permitted. A waiver does not change the concentration.

Greg Lindberg went to federal prison for paying cash to the North Carolina insurance commissioner to get around the same limits. The legal maximum exists because the last time someone exceeded it without permission, they went to prison. Athene exceeds that maximum by 26 times and collects $688 million a year in management fees.

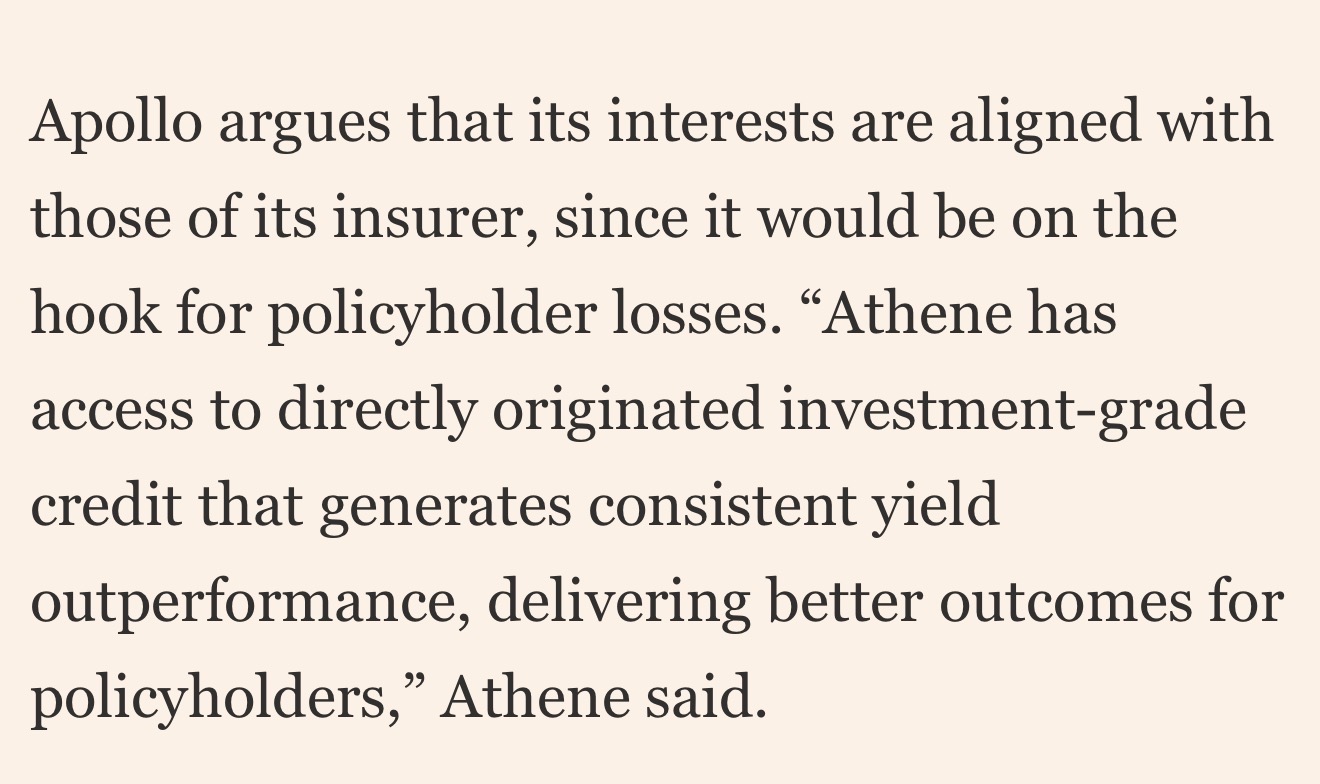

Apollo tells regulators and lawmakers that its interests are aligned with policyholders — that it would be on the hook for losses.

Financial Times, October 31, 2018. "Private equity: Apollo's lucrative but controversial bet on insurance."

Apollo tells regulators its interests are aligned — that it would be “on the hook” for policyholder losses. Apollo tells equity investors the opposite — that Athene’s liabilities are non-recourse to Apollo’s balance sheet. The defense is that these are different legal entities. That is the point. Apollo structured it so that the entity making promises to regulators has no claim on the entity with the money. Alignment is not alignment when the capital is firewalled on the other side of a corporate veil. In receivership, the parent’s resources are typically pursued. The auditors know this. They have not said anything and the investors are clueless.

The $1.54 trillion is only what we can see — the affiliated reinsurance reported in US statutory filings. It does not include the independent cross-pollination. It does not include the retrocession chains. It does not include Europe.

VI. The Three Layers

Gober found the first scheme and went to the regulators. He wrote letters. He filed with the NAIC. He sent certified mail to state commissioners. He screamed. The industry heard him. They did not stop. They moved to the next scheme. He figured that one out. He screamed again. They moved again. Three decades. Three layers of obfuscation. Each one invented because the man in Mississippi would not shut up about the last one. He still has not.

Layer 1: The Captive. The company forms a captive in Vermont or Bermuda. It cedes liabilities but sends far fewer assets. The gap is plugged with XOL paper or contingent letters of credit. There are approximately $600 billion in captive reinsurance in the United States. The only time anyone has ever seen inside, the captives were funded at 3.7 cents on the dollar. The sample is one.

Layer 2: The Cross-Pollination. When the captive layer grew too large, they started ceding to independent troubled companies.

"Massive amounts of reinsurance going to and from only the troubled companies. None of it with New York Life or Northwestern Mutual, none of the good companies, the Guardian, none of them. Only the troubled companies are ceding to and assuming from each other."— Tom Gober

First Allmerica Financial Life Insurance. $100 million in surplus. $22 billion in affiliated reinsurance — a 14,864% ratio. It owes $17 billion to seven independent insurance companies. Metropolitan Life has approximately $10 billion recoverable from First Allmerica. That is more than MetLife's entire statutory surplus of $8.6 billion. If First Allmerica fails, seven independent insurers take losses exceeding their surplus. All of First Allmerica's reinsurance flows offshore to its affiliate — Global Atlantic, controlled by KKR.

Layer 3: The Seven Funnels.

"There are about seven life reinsurance companies in the US. They assume from about 550 independent carriers. No longer are they spreading risk. They’re concentrating it. All of it is going offshore to their affiliate. Suddenly you’ve got 550 carriers filtered through just seven companies and all of it going to a handful of offshore affiliated reinsurers we can’t see."— Tom Gober

Approximately 670 life insurance companies depend on these seven — bound by 831 overlapping reinsurance contracts. Many cedents depend on two or three funnels simultaneously. When one funnel breaks, the same company gets hit from multiple directions. Their combined liabilities to cedents: $149.7 billion. Of that, roughly $400 million was retroceded to real, independent counterparties. The rest — $133.5 billion — went to their own affiliated captives and offshore entities. Bermuda. Barbados. Ireland. No US examiner has ever set foot inside them. The combined surplus of all seven: $6.9 billion. If just 5.2% of the offshore is not recoverable, all seven are insolvent.

Hannover Life Reassurance — 231 cedent companies — is one of the seven funnels. Hannover is also the counterparty on the XOL assets it says it will never pay. The same company writing the phantom contracts is supposed to be the backstop for 231 insurers.

"They have intentionally set up a system that if nothing fails is extremely brilliant. It is the most efficient possible machine. But if one thing goes even slightly wrong, the dominoes are set up so that they’ll all fall."— Tom Gober

The counterargument is that regulators intervene before dominoes fall. The counterargument assumes the regulators can see the dominoes.

Once liabilities land offshore, we know nothing. The primary company cedes to its offshore reinsurer. That reinsurer retrocedes to another company offshore. That company cedes back to an affiliate of the originator. The liabilities do a round robin. Offshore entities do not file Schedule S. Their GAAP statements do not itemize the chain. It is untraceable by design. The offshore total that we can see and that is counted on is approximately $2 trillion. The $1.54 trillion affiliated is a subset. But it is probably multiplied at each step by the same phony premium for pretending that Brookfield paid Hannover.

"Rather than Spreading Risk as Once Intended, It is My Professional Opinion that These 7 Life Reinsurers Have Acted as a Vacuum, Concentrating Risks of 831 Life Insurance Companies Into a Handful of Affiliated Offshore & Captive Reinsurers."— Thomas D. Gober, presentation to the US Senate Banking Committee, March 1, 2023

VII. The Morphine

In 2006, the FBI arrested executives at General Reinsurance Corporation — a subsidiary of Berkshire Hathaway — for a sham reinsurance scheme with AIG. Tom Gober worked the criminal case.

Elizabeth A. Monrad was Gen Re's Chief Financial Officer. A CPA. On November 15, 2000, on a recorded phone call with John Houldsworth — CEO of Cologne Re Dublin, the offshore subsidiary used specifically because it "did not report to anyone" and addressed what the conspirators called "the North American problem" regarding regulators — Monrad described the structures that are the subject of this article:

"These deals are a little bit like morphine. It's very hard to come off of them."— Elizabeth A. Monrad, CFO of General Reinsurance Corporation, recorded November 15, 2000. United States v. Ferguson et al., Case 3:06-CR-137 (D. Conn.), Superseding Indictment, Document 229, Page 21.

In the same indictment, Gen Re's lawyer Robert Graham emailed that the deal should use offshore entities so that "any reviewer of the AIG US entity's statements wouldn't be able to connect the dots to CRD and beyond." Houldsworth asked if the deal would "show up in any kind of public document" in Ireland. He replied: "absolutely not."

When Houldsworth asked another executive "how much cooking goes on" at AIG, the reply was: "they'll do whatever they need to make their numbers look right... they're very meticulous about managing their numbers."

They kept the recordings. That is why they went to prison.

After her conviction, Monrad left Gen Re. She resurfaced at TIAA-CREF — the nonprofit pension insurer that manages retirement savings for teachers and public employees.

Every large insurance group has at least one reinsurer in Dublin, Ireland. Ireland strictly regulates insurance. It does not regulate reinsurance at all. This was established in the court proceedings of the case Monrad was convicted in.

VIII. The Numbers

Total US life and annuity industry surplus: $657 billion.

Three scenarios. Gober’s estimates as brackets.

"If even half is not good, it breaks everybody and it breaks a $10 trillion balance sheet system." (Gober)

| Amount | |

|---|---|

| Affiliated reinsurance | $1,543B |

| x 50% not money good | $770B |

| Industry surplus | $657B |

| Industry is insolvent by | $113 billion |

Half. Just half bad. And it breaks everybody.

The captives at 5% (what we actually saw)

| Amount | |

|---|---|

| Captive reinsurance | $600B |

| Funded at 5% (like Brookfield) | $30B |

| Phantom | $570B |

| Industry surplus | $657B |

Captives alone consume 87% of industry surplus. One bad year finishes it.

"I only trust 30% is money good." (Gober)

| Amount | |

|---|---|

| Affiliated reinsurance | $1,543B |

| x 70% not money good | $1,080B |

| Industry surplus | $657B |

| Industry is insolvent by | $423 billion |

The hole is 1.64x the industry's total surplus.

Strip the affiliated reinsurance credit from each entity’s balance sheet: 29 of the top 30 are insolvent without it. The only question is whether the reinsurance is funded. The one time we saw inside, it was not. The only survivor: MassMutual. A mutual. No PE overlay.

When pressed, the industry will throw Brookfield under the bus. Brookfield is well respected. They are not a leader in this. From what we can see, every one of these firms — from Apollo to Golden Gate — are doing the same things. The only difference is that someone on Brookfield’s tech team did not know what was supposed to stay hidden.

Not included:

- Non-affiliated cross-pollination (Layer 2)

- Retrocession multiplier (round-robin)

- European exposure (Ireland, UK, continent)

- $2 trillion total offshore is what we can see. The rest is dark.

IX. How It Starts

Private credit portfolios are not marked by markets. They are marked by the managers who collect fees on them. The marks do not move until they have to. When a borrower misses a covenant, the manager can waive it. When a borrower cannot cover interest, the manager can capitalize it as PIK — paying interest with more debt instead of cash. When the portfolio looks soft ahead of fundraising, the manager can hold marks steady and let the vintage speak for itself. None of this is illegal. All of it delays the reckoning. One of the primary reasons Enron collapsed was mark-to-market accounting on illiquid markets — booking future profits on contracts that had no observable price. These firms do something worse. They mark to model. They price assets that do not trade using assumptions they choose. Enron at least pretended there was a market. Private credit does not bother.

The reckoning is a downgrade. When enough borrowers miss enough payments that even a conflicted manager cannot hold the marks, the designations change. A downgrade from investment-grade to below-investment-grade is a mechanical trigger on the insurer’s balance sheet. The NAIC designation flips. The capital charge increases. The bond that required almost no surplus yesterday requires multiples of it today.

For a company like Athene — 69:1 leverage, 1.45% margin of solvency — a modest wave of downgrades eats through the capital cushion in weeks. Not years. Weeks. The math is not complicated. If 5% of the portfolio gets redesignated and the capital charge triples on those positions, the surplus is gone. The company needs its reinsurance to be real. It needs to call on the captive.

The captive is funded at 3.7 cents on the dollar. The backstop — Hannover — booked a reserve of zero. The asset that was supposed to absorb the loss does not exist. The insurer was structurally insolvent before the downgrade. Now it is visibly insolvent. The only difference is that someone turned on the lights.

Private credit funds report quarterly, with lags. The primary statutory insurance filings are annual. The deterioration in the underlying loans can be six months old before it shows up on the insurance balance sheet. By the time the NAIC designation changes, the loss has already happened. The system does not provide early warning. It provides late confirmation.

X. The Fed Knows

The Federal Reserve’s own researchers have been documenting this. Carlino, Foley-Fisher, Heinrich, and Verani (March 2025) found that affiliated asset managers now control 72% of the industry — the same $187 billion CLO exposure and the same hidden leverage structures described in the previous section. Their conclusion: life insurer risky debt exposure now exceeds subprime mortgage-backed securities holdings from late 2007. The leverage in joint venture loan fund structures reaches up to 12:1 — despite regulatory limits that appear to show under 2:1.

The Fed’s own FEDS Notes (February 2024): recovery rates on direct loans — 33 cents on the dollar. Interest coverage: 2.0x — and the Fed, like the industry, is using EBITDA, not EBIT. When you add maintenance capex and account for company size, these borrowers are firmly in junk territory. The leverage they are running would be inadvisable for public companies with better asset selection and access to capital. And that is before unadjusting the bogus addbacks that PE sponsors bake into “adjusted EBITDA.” The industry “has yet to endure prolonged recession.” Interconnections with banks pose “hidden risks to the financial system.”

The Boston Fed (2025) asked: “Could the Growth of Private Credit Pose a Risk to Financial System Stability?” The title is the answer.

These are Federal Reserve economists. Publishing under the Fed’s name. And still nothing happens.

XI. The Machine

The sham reinsurance and the dividend extraction are the same event.

"As you approach year end, the CEO calls the CFO and the actuary: Where do we stand? Can we pay our dividend? We're a billion short. The CEO turns to the actuary: I want you to come back with a much lower number."

The actuary uses the 10% variance permitted by the Society of Actuaries. Goes lower. Still not enough. The CEO insists.

"In every criminal case I worked, the actuary literally cried. They told him if he didn't come back with a lower number, he'd have to take his kids out of private school."

Still not enough. That is when they do the first captive deal. Cede a billion in liabilities. Send half a billion in real assets. Plug the hole with XOL. Surplus rises by $500 million. The dividend is paid. The stock goes up. Management compensation is tied to the stock price. Next year the gap is larger. The captive deal must be larger. The morphine dose increases.

The metric designed to catch all of this is Risk-Based Capital. It measures how much surplus a company needs relative to the risk on its books. But the companies control which assets run through the formula. The private credit, the affiliated paper, the illiquid alternatives — none of it touches the RBC calculation. The number comes out clean. The regulator sees a ratio that says the company needs almost no surplus. The ratio is correct. The inputs are a lie.

The inputs include $187 billion in collateralized loan obligations. Life insurers own 17% of the entire US CLO market and 22% of the private credit CLO market. They hold 35 to 50% of the mezzanine tranches — the first paper wiped in a default cycle after equity. Under current NAIC rules, a AAA-rated CLO receives the same capital charge as a US Treasury. It is not a Treasury. It is a leveraged pool of loans to companies that cannot access public debt markets. The private credit CLOs — the ones that PE sponsors originate, package, and place into their own carriers — have not been re-rated at all. Athene holds $6 billion of them. The largest exposure of any insurer tracked. Apollo originates the paper. Apollo manages the portfolio. Athene is the buyer. There is no independent bid. This is the part that is real. And when the underlying loans default, it just disappears.

"The moment private equity buys a carrier, they force it to use them as the asset manager. They look at the portfolio — 'they've got two billion in Treasuries, they only need a billion and a half. Let's swap 500 million of our worst paper for their Treasuries.' Then it gets more sophisticated. They start issuing affiliated notes. A secretary has done these notes for years. All they do is call her, change the dollar amount and the maturity date. Poof, policyholders have junk rammed down their throats."— Tom Gober

Athene’s affiliated investments went from $40 billion to $52 billion in one year. The NAIC limit is 50% of surplus — $2 billion. Athene is at 2,600% of the guideline. Whether Iowa granted a waiver does not change the concentration. It changes the paperwork. Twelve billion dollars moved into affiliated paper in twelve months.

XII. What Happens Next

A widow in Connecticut held a $2 million life insurance policy with PHL Variable. Her husband paid premiums for decades. When PHL entered receivership, the rehabilitator confirmed the XOL assets were worth zero. The state guaranty association stepped in. It covered $300,000 — the cap. Fifteen cents on the dollar. She is not unusual. She is the template.

In the last decade, hundreds of corporations transferred their defined-benefit pension obligations to life insurers through pension risk transfers. The employer is off the hook. The insurer now owes the retiree directly. The retiree’s pension is backed by Athene. Leveraged 69 to 1. Affiliated reinsurance 57 times its surplus. The captive behind it is funded the way Brookfield’s captives are funded. The pension is a claim on 3.7 cents.

The guaranty funds are financed by assessments on surviving insurers. If the surviving insurers are also insolvent — and 29 of the top 30 are, without their affiliated reinsurance — there is no fund. There is no backstop to the backstop.

A teacher in Ohio retires on an annuity. The annuity is held by an insurer. The insurer ceded the risk to a captive. The captive booked a phantom asset from Hannover. Hannover is leveraged 99 to 1 on affiliated paper and backstops 231 other companies with the same structure. The teacher’s retirement is a claim on a chain that terminates in nothing.

Closing

I am not a journalist. I am a citizen and a market participant. I am also a recovering alcoholic who knows what addiction looks like. Someone needs more and cannot stop. This industry needs more fees the way I needed more drinks. It does not end differently because you financially engineered better.

It is fugazi. The backing is either invisible or it does not exist. The counterparty says it will never honor the contract. The NAIC’s own tests say no risk was transferred. The NAIC’s own accounting standards say it is not an asset. Vermont passed a law saying it is. Then Vermont made it confidential. Then Vermont made it immune to subpoena. When a company cedes a billion dollars in policyholder obligations to a captive, sends half a billion in real assets, plugs the remainder with a contract the counterparty says it will never honor, and then pays itself a management fee and a dividend out of the surplus it just manufactured — that is extraction of value from policyholders to shareholders. There is no other word for why this is permitted.

Tom Gober has worked insurance fraud cases for the FBI for over a decade. In every case where forensic accountants went in on day one of a receivership, they recovered the money. Not from the insurer — the insurer was broke. From PricewaterhouseCoopers. From Milliman. From the outside actuarial and accounting firms that signed off on balance sheets they knew were hollow. They paid in a hurry. They did not fight. Because the discovery process would have shown they knew.

The power at stake here is so massive — so concentrated, so politically connected, so deeply embedded in every node of the regulatory and financial architecture — that all I can say is I am good with my God. I do not need to be good with Marc Rowan or Jon Gray or anyone whose net worth depends on nobody reading the footnotes.

I would go broke and live in the woods in Mississippi to stop this madness. All I need is one friend, and his name is Tom.

Once the government fills a trillion-dollar hole with taxpayer money, the incentive to claw back from the architects disappears. That is what they are counting on. The extraction is complete. What remains is the obligation and it falls on policyholders and taxpayers in that order. My generation inherits the wreckage. My children inherit the debt written to clean it up. The downgrades to private credit have already started. Everyone can see them coming. The trigger is not hidden. It is on a schedule. One commission with subpoena power would rip the cover off of this before the downgrades do it for us. For once in the history of American finance we could be proactive. This will blow up. The only variables are when and how much the public pays for it.

Sources:

1. AEL Re Vermont, Inc. — 2024 Annual Statement. NAIC Company Code 17189.

2. AEL Re Vermont II, Inc. — 2024 Annual Statement. NAIC Company Code 17553.

3. AEL Re Vermont III, Inc. — 2024 Annual Statement. NAIC Company Code 17722.

4. Thomas D. Gober, CFE — Presentation to US Senate Committee on Banking, Housing, and Urban Affairs. March 1, 2023.

5. S. Hrg. 117-747, at 57. Senate Committee on Banking, Housing, and Urban Affairs, "Current Issues in Insurance" (September 8, 2022).

6. Thomas D. Gober — Expert Declaration, US District Court, District of Maryland (May 28, 2024). Lockheed Martin pension risk transfer litigation.

7. NAIC/SNL Financial YE 2025 — Affiliated reserve credits and modified coinsurance, all 714 US L&A carriers.

8. NAIC/SNL Financial YE 2025 — Surplus, liabilities, and total assets, all US L&A carriers.

9. United States v. Ferguson et al., Case 3:06-CR-137 (D. Conn.), Superseding Indictment, Document 229, filed September 20, 2006.

10. FSOC 2025 Annual Report. Financial Stability Oversight Council.

11. IMF Global Financial Stability Note 2023/001.

12. BIS Papers No. 161 (October 2025).

13. NAIC SSAP No. 4 — "Assets and Nonadmitted Assets."

14. Vermont Statutes Annotated, Title 8, Chapter 141.

15. John Ellis, "Warnings of Mounting Risk," News Items Substack. November 15, 2025.

16. United States v. Greg E. Lindberg, Case No. 3:19-cr-00095 (W.D.N.C.).

17. Koijen & Yogo, "Shadow Insurance," Econometrica Vol. 84, No. 3 (2016).

18. The Real Eisman Playbook, Episode 48. Steve Eisman and Thomas D. Gober. March 2, 2026.

19. Hannover Life Reassurance Company of America — Annual Statement (public filing).

20. Carlino, Foley-Fisher, Heinrich, Verani — Federal Reserve FEDS Notes. March 21, 2025.

21. Newsweek — "The Next AIG Scandal?" Michael Hirsh. March 18, 2009.

22. Barclays Research — "US Insurance and CLOs: NAIC CLO Proposal Skews More Negative to RBC Ratios than Positive." March 30, 2026.

23. Financial Times — "Private equity: Apollo's lucrative but controversial bet on insurance." October 31, 2018.